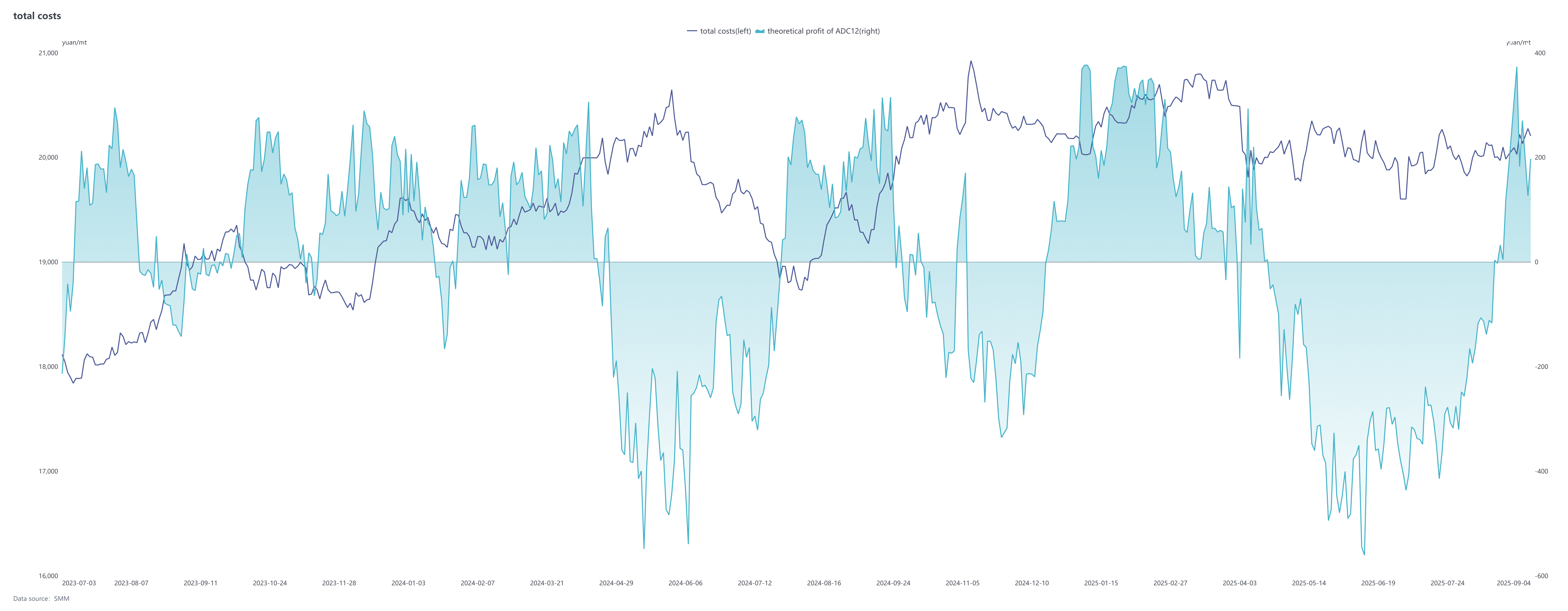

Futures side, the most-traded cast aluminum alloy 2511 contract fluctuated upward in August, rising continuously from the low of 19,800 yuan/mt at the beginning of the month to a record high of 20,555 yuan/mt. As of September 5, it closed at 20,280 yuan/mt. Spot side, ADC12 prices generally followed the upward trend but not the downward movement in August, with the price center rising rapidly. The inverted spread against A00 aluminum prices continued to narrow, ending the three-month inversion pattern on August 29 and shifting to a small premium. As of September 5, SMM ADC12 prices rose by 750 yuan/mt to 20,750 yuan/mt compared to early August, with the theoretical premium against the most-traded futures contract expanding to around 520 yuan/mt. The average ADC12 price in August increased by 1.3% MoM from the previous month.

Cost support was significant, as domestic and international aluminum scrap supply remained tight, with aluminum scrap prices rising rapidly in tandem with aluminum prices. Meanwhile, prices of auxiliary materials such as silicon and copper edged up. Additionally, the No. 770 document issued by four ministries triggered adjustments to tax rebate policies, with many regions canceling tax refunds and potential back-tax risks further increasing corporate cost pressure. The strong willingness to pass on costs drove the rise in finished alloy prices, improving the industry's theoretical profitability.

Demand side, end-use consumption slightly weakened in August as downstream enterprises collectively took summer breaks with subdued purchase willingness. Delivery brand enterprises continued to implement previous orders, providing some support to overall orders. Approaching month-end, market expectations for the September peak season strengthened, driving modest demand recovery. However, rapid spot price increases resulted in active inquiries but limited actual transactions. Entering September, market demand continued rising, with multi-sector consumption recovery steadily boosting secondary aluminum alloy plants' orders, though actual peak-season performance remains to be verified.

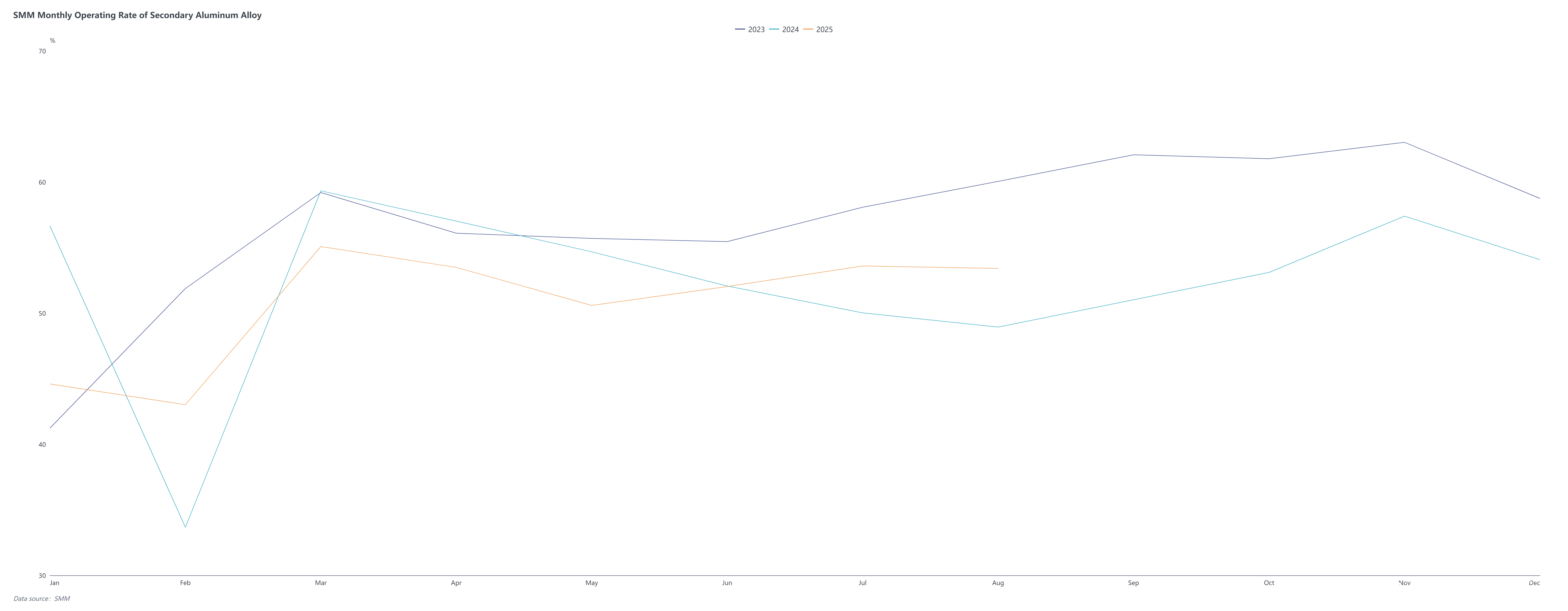

Supply side, the operating rate in the secondary aluminum alloy sector fell 0.19 percentage points MoM to 53.41% in August, up 4.67% YoY. The overall downward trend stemmed from tight raw material supply, insufficient new orders, compressed production margins, and policy adjustments. Regional production halts or cuts occurred in Anhui and Jiangxi due to tax policy revisions, while environmental protection inspections reduced output in Hebei and Jiangxi. However, large enterprises and delivery brand producers maintained relatively full order books, operating at consistently high capacity utilization rates with minor improvements at some facilities, driving significant YoY growth in overall operating rates. Entering September, seasonal consumption recovery is expected to lift operating rates, though constraints persist including unclear local tax rebate policies prolonging market wait-and-see sentiment, aluminum scrap procurement difficulties, and high raw material costs. Long-term, as automakers enter their year-end push for annual targets, the sector's operating rate is projected to sustain its recovery trend in Q4.

Overall, in August, prices were more likely to rise than fall amid strong cost support and policy disruptions, but weak end-use demand and inventory buildup pressure limited the upside room. Looking ahead to September, high costs, policy pressure, and low inventory will continue to support aluminum prices fluctuating upward. If seasonal demand picks up as expected and policy impacts deepen, prices may break through the current range. However, the extent of demand recovery remains a key constraint, requiring close attention to policy implementation progress, the recovery of aluminum scrap supply, and marginal changes in end-use demand.